Stressless “Stress” Tests for Wall Street’s Banks Endanger Main Street Families, Businesses, and Community Banks

By Shayna Olesiuk, Director of Banking Policy, and Dennis Kelleher, Co-founder, President and CEO

Last month, the Federal Reserve reported that its annual stress test showed that the country’s largest banks could all endure a severe recession. This sounds like positive news that should be celebrated, right?

Wrong. The truth is that these results spread false comfort from what has become a flawed and weakened stress testing exercise, which results in banks having too little capital. That’s critical because the only things standing between a failing bank and a taxpayer bailout is the amount of capital a bank has to cover its own losses. It’s like the amount of money a family has set aside for emergencies – if it’s not enough, then they can’t pay an unexpected bill.

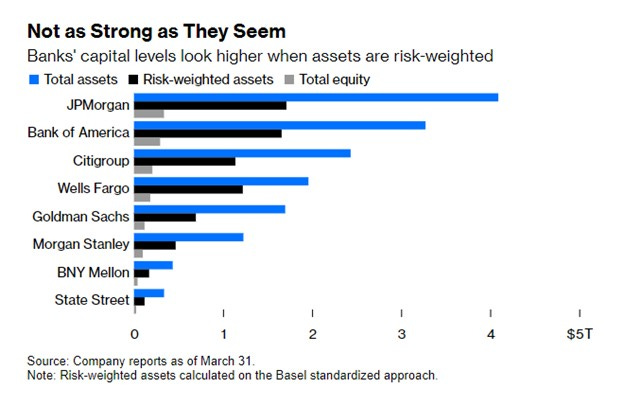

That’s what happened last year when 3 of the 4 largest bank failures in U.S. history happened. Those banks didn’t have enough capital (a banks’ “emergency savings”) to cover their losses, so the government had to step in and inject $40 billion in capital to prevent a banking crisis. The problem isn’t limited to those banks. None of the big banks have enough capital, as was pointed out in a recent editorial and as made clear by this chart:

That’s why the stress tests reveal much more about the inadequacy of the tests than the resilience of our financial system and its ability to weather a crisis. The fact that banks “sailed through” the tests is a red flag they are not very tough. Making matters worse, the tests set the minimum amount of capital a bank has to have, which enables them to eject any amount of capital above that lowest level – that’s why banks announce higher shareholder buybacks and dividends right after the stress tests. That results in banks’ having the bare minimum in “emergency savings” when the unexpected happens. Thus, stress tests have been perverted into capital ejection mechanisms and result in banks that have too little capital as revealed in the chart above.

Protecting the American people from devastating financial crashes and future bank bailouts with minimum levels of capital is a dangerous, high-risk gamble, and, frankly, irresponsible. This is particularly true given stress tests are based on the impossible premise of regulators guessing how a severely stressed scenario will play out in the future, which they have failed miserably at in the past (including as recently as last year!).

Simply put, the Fed has weakened the stress tests since 2017 to the point that they are not stressful enough. Therefore, the results lull policymakers, regulators, banks, and the public into a false sense of security, providing a smokescreen that obscures enormous threats to our financial system. The American people should not take comfort in the results as they relate only to a predictable recession scenario, triggered by known historical drivers. After all, we know that banking stress, failures, and crises are almost always not as predicted and, therefore, such test results are of limited value.

While the post-2008 financial crisis reforms have not come close to removing the Damocles Sword of Wall Street’s too-big-to-fail banks problem as the law requires, they did substantially strengthen the U.S. banking system by ratcheting up the regulation and oversight of the largest banks. Indeed, post-crisis banking sector reforms are the key reason the largest banks entered the COVID-19 pandemic in relatively strong financial condition. Remarkably, all this was done while bank lending increased, and bank profits skyrocketed. Financial reform proved to be a win-win.

Nevertheless, many of the reforms have been under attack by the banking industry and a number of these reforms have been seriously weakened by legislation, rulemaking, and reduced supervision. As a result, banks that present systemic risks and threaten financial stability have been able to evade the stronger oversight and regulation and consequently continue to threaten Main Street Americans and businesses. That was proved by the collapse and bailout of Silicon Valley Bank, Signature Bank, and First Republic Bank in 2023.

Although many of the post-financial crisis reforms remain intact for the very largest banks (those classified as Global Systemically Important Banks or “GSIBs”), there have been significant changes that undermine the value of what is perhaps the most important post-crisis initiative—the Fed’s stress testing program and related banking supervision efforts.

These changes include:

· The size of banks that are subject to the stress tests was increased;

· Assumptions in the stress tests were weakened;

· The leverage ratio requirement was removed;

· The qualitative assessment—a critical component of the overall stress testing program—was effectively eliminated; and

· Stress test models were made more transparent and thus more vulnerable to gaming.

Importantly, the current stress tests are based on scenarios and economic projections that are rooted in past recessions. During each of these historical periods, the banks and other sectors of the economy were the beneficiaries of enormous amounts of government support. Instead, the stress tests should be revised to contain sufficiently severe scenarios that would actually test banks’ resilience in a situation where they have to stand on their own – without any government assistance. The stress tests need not predict every potential bad outcome, but they must be sufficiently severe to show that the banks are strong enough to withstand a range of bad outcomes—including those that the Fed and banks may have not even conceived.

That’s why we recommend that the Fed should reinvigorate and strengthen the stress tests and expand the stress tests to include more scenarios with capital implications.

The failures of multiple large banks in 2023 illustrate the unacceptable and unknown risks that remain in the banking system and that undercapitalized banks bring severe risks and consequences. The bailouts of Silicon Valley Bank, Signature Bank, and First Republic Bank cost Americans $40 billion because these three banks did not have enough capital. Worse, the stress testing process was blind to this risk, primarily because of deregulatory changes and unwarranted assumptions (in addition to egregious mismanagement and supervisory failures).

The bottom line is that the Fed’s stress tests should be strengthened; the deregulation that happened starting in 2017 should be reversed; and all large banks should be required to undergo genuinely stressful tests. Thereafter, they should be required to have more than enough capital – not the minimum amount - to ensure that they will not fail, cause a crash, and result in Americans paying to bail them out—again.

Learn more in our recently released Fact Sheet on Stress Tests.

Excellent article. Thank you. Sadly, I doubt there is political will to protect main Street from another banking debacle. We're seriously backsliding and it's going to worsen.