The Capital One-Discover Merger Should Be Rejected Because Supersizing More Dangerous Banks is Bad for Main Street Americans

By Shayna Olesiuk, Director of Banking Policy, and Dennis Kelleher, Co-Founder, President and CEO

“We don’t exist to serve banks; banks exist to serve us,” said the head of the banking regulator at the OCC recently. While most Americans undoubtedly agree with that, too often Washington policymakers and regulators don’t act like they agree. Well, they now have the perfect opportunity to prove that they get it because they have to review and decide whether to approve a proposed merger between two of the largest financial institutions in the country. It should not be a difficult test because the merger would create yet another dangerous too-big-to-fail megabank and they both have long histories of illegal, deceptive, and unfair actions. If those banks exist to serve us, they have failed, and the merger should be rejected.

Earlier this year, Capital One announced it would acquire Discover in an all-stock transaction worth $35.3 billion. The merger would combine the 10th largest bank with the 26th largest bank to create the 6th largest bank. It would also create the largest credit card issuer in the U.S., with more than $200 billion in credit card loans outstanding.

The proposed merger will harm Main Street Americans who already have the deck stacked against them. The merger will reduce competition, provide less choice, enable higher fees and costs, and cause job losses. Approval of the merger would hurt consumers and small businesses, erode competition, endanger financial stability, and allow two banks with an egregious history of inadequate management, excessive risk-taking, and repeated illegal behavior to grow even larger and more interconnected.

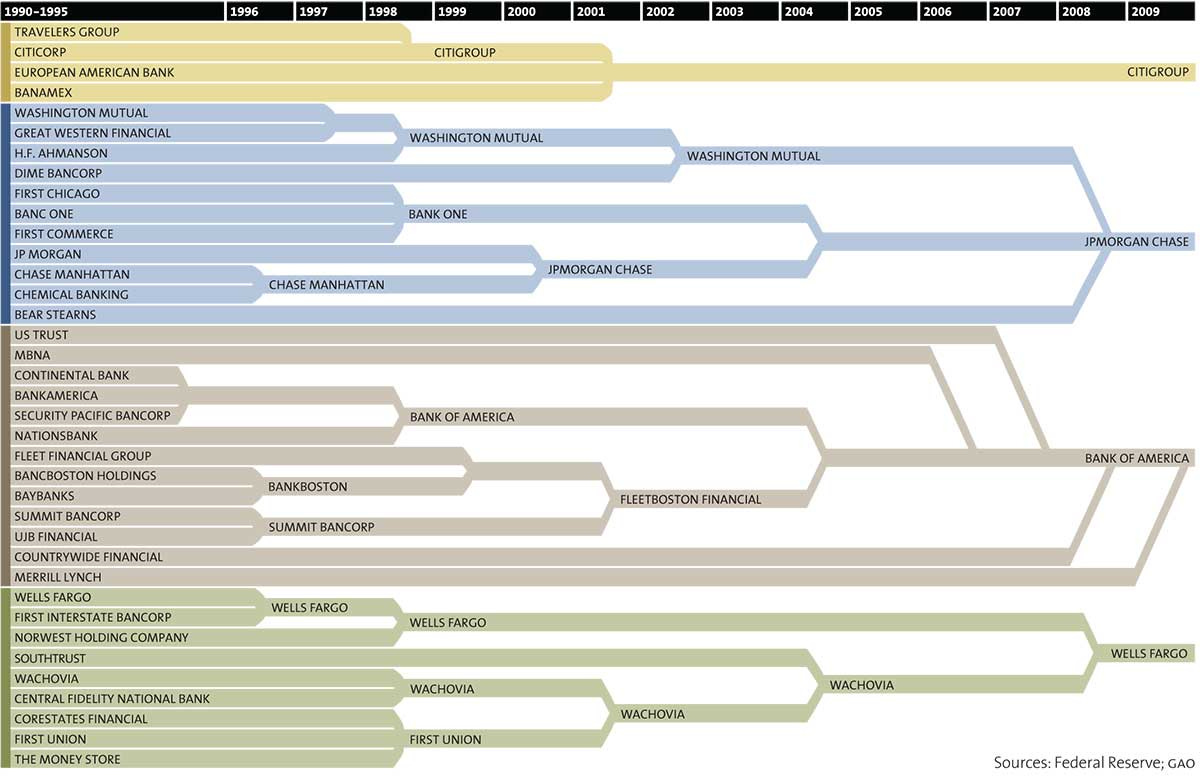

The merger of these two giant financial firms into the 6th largest megabank would be on top of decades of policymakers and regulators allowing too many banks to merge and create the too-big-to-fail crisis that fueled the 2008 financial crash and that caused economic devastation across this country. That happened because of a very weak merger review process, combined with changes in laws and economic events, which contributed to massive and unnecessary consolidation in the banking industry (see Chart 1). Not only would the proposed merger create another too-big-to-fail megabank, but it would also dramatically increase the market power of Capital One through the acquisition of the Discover payment network. In short, Capital One would have enormous power to overcharge customers for everyday credit card transactions and it would leave working Americans with fewer choices for credit card providers than ever.

Research shows that larger credit card issuers consistently charge higher interest rates to consumers regardless of how good their credit ratings are and Capital One is already among the highest-priced credit card issuers in the country with interest rates on credit card products above 30%.

The increased market concentration from this merger will almost certainly lead to higher credit card interest rates and higher fees charged to consumers. In fact, in 2023 alone, banks moved $233 billion in interest and fees on credit card lending from the pockets of consumers into the pockets of those banks (see Chart 2). This is up from an average of $135 billion from the past decade.

Moreover, late fees are consistently the biggest category of fees for credit cards (exceeding even annual fees from people having the card in the first place!) (see Chart 3). Of course, those are paid by the poorest Americans who can’t pay their bills on time and can least afford the late fees.

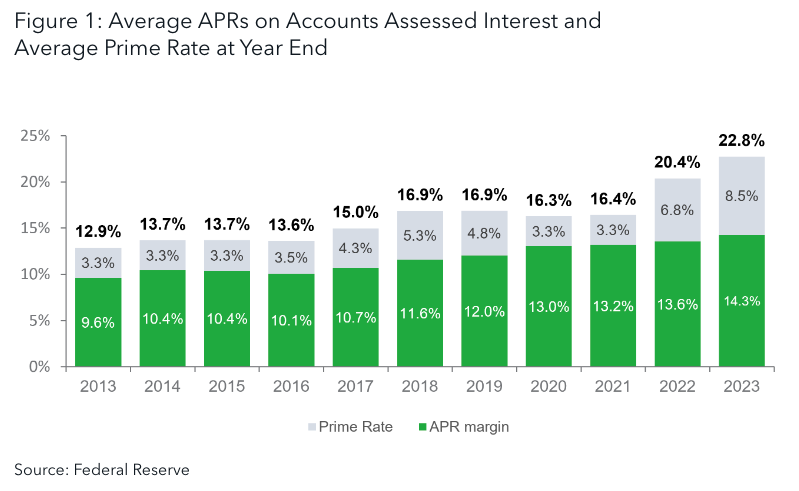

Adding insult to injury, the Consumer Financial Protection Bureau reported that credit card interest rate margins are at all-time highs, jumping from 16.4% in 2021 to 22.8% in 2023 (see Chart 4)! Thus, while the Fed raised rates, banks took advantage of that to increase the fees they extracted from consumers. So not only didn’t they pass along the higher rates to their savers, but they hit their credit card customers with significantly higher rates at the same time.

When inflation is added in, it’s no wonder—as CNN reported—that 39% of Americans worry “most or all of the time” that they can’t pay their bills! That share rises to 46% for Black Americans, 52% for Latino Americans, and 55% for Americans making less than $50,000 per year. Many of those Americans are unable to pay their bills and turn to the most readily available lifeline—credit cards—to fill the gap. But rather than extend a helping hand, the credit card companies are extracting even more wealth from hardworking and hard-pressed Americans, resulting in increasing anxiety, inequality, and wealth gaps.

Rubbing salt in consumers’ wounds, both Capital One and Discover have a long history of illegal, willful, deceptive, and unfair actions that have repeatedly consumed regulatory attention and often resulted in fines for both banks. This includes Capital One willfully failing to implement an effective anti-money laundering program, for which it paid $390 million in civil penalties in 2021.

Under the law, Congress intended the banking agencies to deny mergers that “in any respects” fail to meet public interest objectives concerning convenience and needs, managerial resources and future prospects, and financial stability. There is no question that this proposed merger fails all three considerations and amply justifies—if not mandates—regulators to deny it.

Learn more in Better Markets recent comment letter on the proposed merger.