The Risks of Private Credit ETFs for Retail Investors

By Benjamin Schiffrin, Director of Securities Policy

As we detail in our new report, private markets present real challenges for investor protection and capital formation. That’s because much of the growth of the private markets comes at the expense of the public markets, which are deep, liquid and the envy of the world. One reason for this is the public markets have rigorous disclosure requirements, which protect investors and help them determine where to invest their capital. So the public markets provide investment opportunities for investors worldwide and facilitate the efficient allocation of capital to American and global businesses. Indeed, a recent study found that public markets allocate capital much more efficiently than private markets.

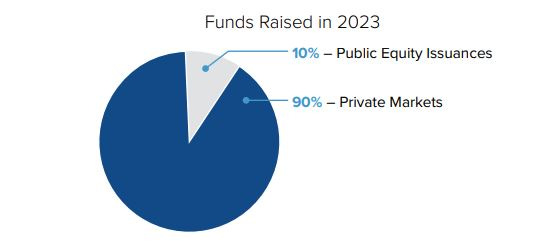

Nonetheless, over the last several decades, Congress and the SEC have steadily expanded the exemptions that permit private offerings free from the registration and disclosure requirements that govern public offerings. This has led to explosive growth in the private markets. The aggregate amount of capital raised in the private markets has surpassed the aggregate amount of capital raised in the public markets every year since 2017, and the amount of money raised in the private markets now dwarfs that of the public markets.

Up until now, the expansion of the private markets has focused on allowing companies to raise more and more money from sophisticated investors without having to go public. But the private markets now want to expand to retail investors. And a key piece of that move is the financial industry’s push to introduce private credit exchange-traded funds (ETFs).

Supporters claim these ETFs will “democratize” access to private markets, but the reality is much more complicated and potentially much more dangerous for everyday investors.

What Are Private Credit ETFs?

ETFs have long been a popular investment vehicle because they allow investors to buy into diversified portfolios that track an index or sector, typically with low costs and high liquidity. For retail investors, ETFs provide an easy, efficient way to gain exposure to a wide range of financial markets. Now, some asset managers are attempting to offer private credit ETFs—funds that expose retail investors to the private credit markets.

Private credit is a segment of the private markets, meaning it’s not publicly traded and generally remains inaccessible to ordinary investors. Private credit funds usually raise capital from wealthy individuals and institutional investors to make loans to companies. These loans are often illiquid and hard to value. That’s why investors in private credit are usually sophisticated market participants. Institutional investors are able to undertake the due diligence necessary to understand an investment in the private credit markets.

Now, the push for ETFs that expose retail investors to private credit markets is being marketed as a way to “democratize access” to high-yield assets. The proponents of these ETFs say that they will allow average Americans to access the same supposedly lucrative deals once reserved for the ultra-wealthy and Wall Street insiders. But even the most sophisticated investors such as Ivy League university endowments sometimes struggle in the private markets. So while increasing retail investor access to private credit sounds appealing on paper, the reality is that for retail investors private credit ETFs carry enormous risks—risks that could have serious consequences for investors who aren’t aware of what they’re getting into. Let’s take a closer look at why.

The Liquidity Mismatch

One of the key features of most ETFs is their liquidity. Investors can buy or sell shares of the fund throughout the trading day, providing the flexibility to move in and out of investments quickly. But private credit is fundamentally different. Private credit funds are composed of illiquid loans, which are difficult to value and often difficult to sell. So it is unclear how retail investors could easily withdraw money from funds loaded with illiquid assets.

A private credit ETF built on a portfolio of such loans also creates a mismatch between the liquidity expectations of retail investors and the actual liquidity profile of the underlying assets. This mismatch can lead to significant problems if retail investors incorrectly assume that they can easily sell their shares in a private credit ETF. Retail investors may be harmed if they do not understand the risks in the illiquid asset class that is private credit.

Opaque, Risky Assets

Another problem with private credit ETFs is the opacity of the underlying assets. Because private loans rarely trade, fund managers do not have market data to rely on for objective valuations. This means that nobody really knows how to value the loans.

The absence of a consensus as the loans’ value could be hiding loans that are in trouble. Investors could be left in the dark or potentially misled if a private credit fund has been overly optimistic about its portfolio. As a result, the inherent difficulty of valuing non-traded loans could expose retail investors in private credit ETFs to unforeseen losses.

Protecting Retail Investors

The rapid growth of private credit markets has already raised alarms. The International Monetary Fund (IMF) has called for more robust oversight of private credit funds to address the risks posed by their opacity, illiquidity, and potential for systemic instability. But introducing private credit ETFs could exponentially increase those risks by giving more retail investors exposure to an asset class with which they are unfamiliar.

The argument that allowing more investors to participate in a previously inaccessible market will democratize finance has echoes of past marketing campaigns that downplayed risk in the pursuit of profits. For example, Robinhood, which claims to be democratizing finance, has been criticized for pushing inexperienced investors into high-risk products, like options trading, without adequately warning them of the dangers. This kind of marketing has led to disastrous consequences for many users, particularly those with little to no investment experience. By some estimates, between November 2019 and June 2021, retail investors lost over $2 billion trading options. Similarly, the push to introduce private credit ETFs and sell them to retail investors could expose a new generation of investors to the same kinds of risky assets they aren’t prepared to understand or manage.

As we’ve seen from past financial crises, when risky assets are marketed as accessible to everyone—without proper oversight—ordinary investors are often the ones who suffer. While private credit ETFs may sound like an attractive way to diversify a portfolio, they potentially come with a heavy price. Retail investors must be fully aware of the risks before diving into these products, and policymakers must step up to ensure that adequate investor protections are in place to guard against a repeat of past financial disasters.

You can find our report on private markets here.